Beauty Tools & Accessories

Are Young People Screwed?

Jun

Every generation thinks the next one is either lazy, doomed, or somehow both. Young people today get accused of not wanting to work, not wanting to buy homes, not wanting to have kids, and not wanting to answer phone calls from unknown numberswhich, to be fair, is the most reasonable social boundary humanity has ever invented.

But behind the jokes is a serious question: are young people screwed? In the United States, many Gen Zers and younger millennials are entering adulthood with expensive housing, student debt, unstable career ladders, climate anxiety, loneliness, and a cost of living that makes a grocery receipt look like a ransom note. At the same time, young adults are more educated, more flexible, more digitally skilled, and more willing to challenge broken systems than many generations before them.

So the honest answer is: young people are not hopelessly doomed, but they are playing on a harder difficulty setting. The old adult-life scriptgraduate, get a stable job, buy a house, marry, have kids, retire comfortablystill exists, but it now requires better timing, more family support, higher income, lower debt, and sometimes a small miracle involving interest rates.

The Economy Is Not Broken for EveryoneBut It Feels Broken to Many Young Adults

One reason this debate gets messy is that the economy can look strong from 30,000 feet and brutal from a studio apartment. National employment may be solid, wages may rise in some sectors, and the stock market may keep doing its mysterious rich-person weather dance. Yet a 24-year-old trying to pay rent, car insurance, groceries, loan payments, and health care may still feel like the math was designed by a villain.

According to recent Federal Reserve data, about 73 percent of U.S. adults reported that they were doing okay financially or living comfortably, but the same report noted meaningful declines for some groups, including young adults. Price increases remained the most common financial concern, with more than 9 in 10 adults calling them at least a minor concern. That matters because young people usually have fewer assets, smaller emergency funds, and less protection against sudden costs.

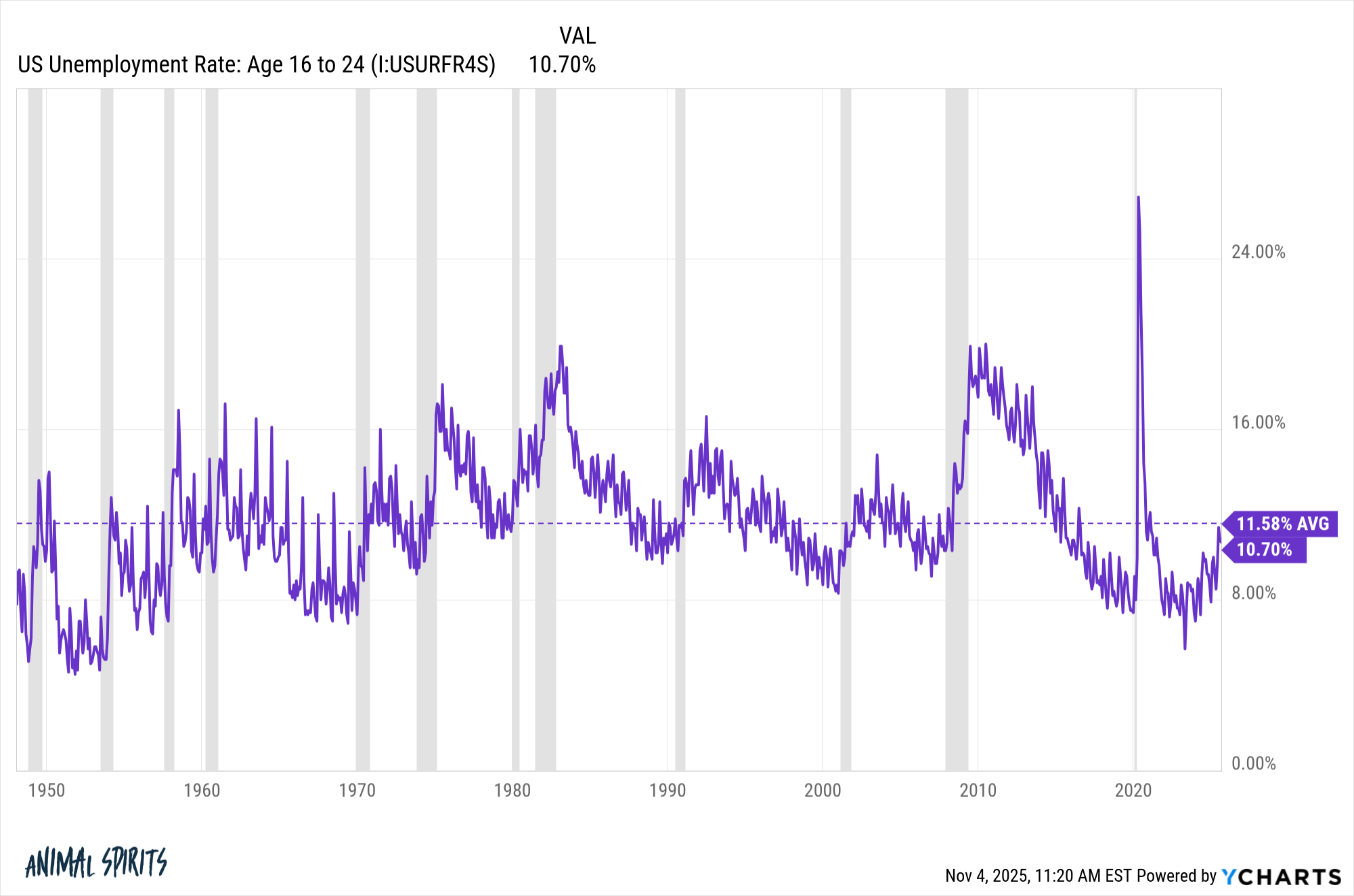

The Bureau of Labor Statistics shows that full-time workers ages 20 to 24 earned much less, on average, than workers ages 25 to 34, and both groups generally earned less than workers in their peak earning years. That is normal in a career cycle, but it becomes painful when entry-level wages meet peak-level rent.

Housing Is the Big Boss Level

If young people sound dramatic about housing, it is because housing has become dramatic. The Harvard Joint Center for Housing Studies reported that U.S. home prices were up roughly 60 percent nationwide since 2019 as of early 2025. Add elevated mortgage rates, high insurance costs, property taxes, and limited starter-home supply, and homeownership starts to look less like a milestone and more like a luxury subscription with a roof.

The National Association of Realtors reported that first-time buyers made up only 21 percent of homebuyers in 2025, a historic low, while the median age of a first-time homebuyer rose to 40. That is a huge cultural shift. For decades, buying a first home was marketed as something you did around marriage, career stability, and maybe after arguing with your spouse about beige paint. Now, many people are still trying to save for the down payment while their rent climbs faster than their patience.

Living With Parents Is Not Failure Anymore

Pew Research Center found that in 2023, 18 percent of adults ages 25 to 34 lived in a parent’s home. A majority of young adults in that situation said it helped their finances. This is not just a “kids these days” story. It is a rational response to a market where rent, deposits, utilities, and moving costs can swallow a paycheck before the Wi-Fi router is even plugged in.

Living at home can come with awkward moments, of course. Nobody dreams of being 29 and whispering, “I’m back,” while carrying laundry past their childhood trophies. But financially, multigenerational living can be a smart strategy. It can help young adults save, pay down debt, support family members, or avoid signing a lease that turns their budget into confetti.

Student Debt Still Shapes the Starting Line

College can still pay off, but the path is no longer simple. The wage premium for a degree remains real, especially in fields with strong demand. But tuition, borrowing, uneven outcomes by major, and the complexity of repayment have made higher education feel like both an opportunity and a trapdoor.

The Federal Reserve reported that the median amount of education debt among people with outstanding debt for their own education was between $20,000 and $24,999 in 2024. That may not sound catastrophic compared with six-figure horror stories, but even a moderate loan payment can delay savings, home buying, business creation, marriage plans, or the ability to quit a bad job. Debt also changes psychology. A person with student loans may not simply ask, “What do I want to do?” They ask, “What can I afford to risk?”

The bigger problem is not only the debt itself. It is debt combined with high rent, expensive transportation, uncertain employment, and a job market that often requires experience for entry-level roles, which is the professional equivalent of asking a newborn to provide references.

The Job Market Is Changing Faster Than Career Advice

Young workers are entering a labor market shaped by remote work, artificial intelligence, contract jobs, automation, and employers that want candidates to be “self-starters” with five years of experience in a software tool invented last Tuesday.

Brookings has noted that research on AI and labor markets is still early, but some evidence suggests young workers in highly AI-exposed occupations may face more pressure than older workers. The World Economic Forum has also projected major labor-market churn, with millions of jobs changing as technology transforms industries. That does not mean every young person should panic and become a goat farmer. It does mean that career planning now requires constant skill updates, networking, adaptability, and the emotional resilience of a customer-service representative on Black Friday.

The Good News: Young Workers Are Adaptable

Young people are often better positioned to learn new tools, switch industries, build online portfolios, and use digital platforms. They are also less likely to accept the idea that loyalty to one employer should be rewarded with a pizza party and a 2 percent raise. Many are questioning old workplace norms, pushing for flexibility, and refusing to treat burnout as a badge of honor.

That matters. The future of work may be unstable, but it is also more open to unconventional paths: certificates, apprenticeships, creator businesses, remote freelancing, community college routes, trade careers, and hybrid work. The challenge is making those paths financially safe enough for more people to try.

Family Formation Is Getting Delayed, Not Deleted

Young adults are not necessarily rejecting marriage, children, or long-term commitments. Many are delaying them because the price tag is terrifying. Pew and Census analyses show that young adults are reaching traditional milestones later than previous generations. The Census Bureau reported that less than a quarter of adults ages 25 to 34 had reached four classic milestonesliving outside the parental home, working, being married, and having childrenin 2024, down from nearly half in 1975.

Child care is another giant factor. Child Care Aware of America found that child care prices rose 29 percent from 2020 to 2024, outpacing overall inflation during that period. For young families, this is not a lifestyle inconvenience. It is a career decision, a housing decision, and sometimes a “Can we afford a second child or even a first?” decision.

When people delay kids, older generations often ask, “Why don’t young people want families?” A better question might be: “Why did we build a society where daycare can cost as much as a second rent payment?”

Mental Health Is Part of the Economic Story

Money is not the only issue. Young people are also dealing with high levels of stress, loneliness, and uncertainty. The CDC reported that in 2023, 40 percent of high school students experienced persistent feelings of sadness or hopelessness, and 20 percent seriously considered attempting suicide. While that data focuses on teens, it shows the emotional environment many young people carry into adulthood.

The U.S. Surgeon General has also warned about loneliness and isolation, noting that roughly half of U.S. adults report loneliness, with some of the highest rates among young adults. This is especially important because modern life can be connected and lonely at the same time. You can have 800 followers, 14 group chats, three dating apps, and still feel like nobody would notice if you disappeared except your phone carrier.

Economic pressure worsens mental health, and poor mental health makes economic progress harder. It is difficult to negotiate a salary, complete a degree, start a business, or move cities when your nervous system is constantly screaming, “Maybe we should just lie on the floor.”

Climate Anxiety Is Not Imaginary

Young people also face a future shaped by climate risk. NOAA data show that the United States experienced hundreds of billion-dollar weather and climate disasters from 1980 through 2024. Rising insurance costs, wildfire risks, floods, heat waves, and storm damage are not abstract problems for people deciding where to live, work, or raise families.

Climate anxiety is not just worrying about polar bears, although polar bears deserve better public relations. It is worrying about whether your city will remain affordable, whether your home will be insurable, whether summer outdoor work will be safe, and whether political leaders can plan beyond the next election cycle.

So, Are Young People Actually Screwed?

Nobut many are squeezed. That distinction matters.

“Screwed” suggests there is no agency, no path forward, and no point trying. That is not true. Young people are building careers, communities, families, startups, art, activism, and wealth. Many are finding creative ways to live well: sharing housing, moving to cheaper cities, using public libraries and free learning tools, building side incomes, choosing trades, negotiating remote work, and rejecting status symbols that no longer make financial sense.

But “not screwed” does not mean “fine.” The systems around young adults need serious repair. Housing supply needs to increase. Wages need to match productivity and living costs. Student loan repayment needs to be simpler and fairer. Child care needs to be treated like economic infrastructure. Mental health care needs to be accessible. Entry-level jobs need actual entry points. And climate adaptation needs to be more than a press conference with a reusable water bottle.

What Young People Can Do Right Now

Young adults should not have to personally fix decades of policy failure with a budgeting app. Still, there are practical moves that can help.

Build Skills That Travel

Focus on skills that work across industries: writing, data analysis, sales, project management, coding basics, financial literacy, public speaking, negotiation, and AI-assisted productivity. A specific job may disappear, but portable skills make career pivots easier.

Treat Housing as a Strategy, Not a Status Symbol

Renting is not failure. Living with roommates is not failure. Moving home temporarily is not failure. The goal is not to impress strangers with your address. The goal is to keep enough financial oxygen to build the next stage of your life.

Use Community as an Economic Tool

Friend networks, family support, mutual aid, professional groups, alumni associations, and local communities can help with jobs, housing leads, emotional support, childcare swaps, and referrals. Individualism is expensive. Community is underrated compound interest.

Vote Like Your Rent Depends on It

Because it often does. Local elections shape zoning, transit, housing development, public colleges, childcare funding, climate resilience, and labor protections. Young people who feel ignored by politics have a pointbut being ignored gets easier when you do not show up.

Experiences Related to the Question: “Are Young People Screwed?”

Imagine a 26-year-old named Maya. She did everything she was supposed to do. She went to college, worked part time, graduated with debt that looked manageable on paper, and landed an entry-level marketing job. Her parents congratulated her. Her professors told her she had a bright future. Her landlord, unfortunately, also had dreamsmostly involving raising rent by $300 a month.

Maya’s paycheck looked respectable until the deductions arrived. Federal taxes, state taxes, health insurance, student loan payments, groceries, phone bill, transportation, rent, utilities, and one emergency dental visit later, her “adult salary” had the flexibility of a frozen waffle. She was not irresponsible. She was not buying gold-plated sneakers or ordering champagne for breakfast. She was simply discovering that adulthood now comes with subscription pricing.

Then there is Jordan, 31, who moved back home after a breakup and a layoff. At first, he felt embarrassed. His childhood bedroom still had a faded sports poster on the wall and a drawer full of old phone chargers that belonged in a museum. But after six months, he had rebuilt his emergency fund, helped his parents with groceries, and completed a certificate program that led to a better job. Moving home was not a step backward. It was a reset button.

Or consider Elena and Marcus, a couple in their early 30s who want a child but keep postponing the decision. They are not anti-family. They are anti-bankruptcy. Between rent, health insurance, car payments, and the cost of infant care in their city, parenthood feels less like a beautiful next chapter and more like signing a contract written in invisible ink. They love the idea of bedtime stories. They are less excited about paying a childcare bill that could bench-press their mortgage dreams.

These stories are common because the pressure is not only financial. It is emotional. Young people often feel judged for not reaching milestones that became harder to reach. They are told to save more, hustle more, network more, sleep more, exercise more, care less, care more, be ambitious, be grateful, and somehow avoid burnout while answering emails with “Happy to help!” when they are absolutely not happy to help.

The experience of being young today is often a strange combination of opportunity and exhaustion. A person can learn almost anything online for free and still be unable to afford the apartment where they would like to sit and learn it. They can build a business from a laptop and still lose momentum because health insurance is tied to employment. They can connect with people across the world and still struggle to make close friends in their own city.

But there is another side to the experience. Young people are rewriting success. Many are choosing mental health over prestige, flexibility over corner offices, community over consumerism, and purpose over performative busyness. They are talking openly about therapy, salary transparency, burnout, climate responsibility, and financial boundaries. They are less willing to pretend that a broken system is a personal character test.

That does not mean everything will magically work out. Optimism is not a substitute for affordable housing. But despair is not a plan either. The most realistic view is that young people are facing real structural obstacles while also developing new survival skills. They are not weak for struggling. They are not doomed for delaying milestones. They are adapting to an economy that changed the rules and then acted surprised when everyone stopped playing the old game.

So, are young people screwed? Not permanently. But they are under pressure, and pretending otherwise is lazy analysis. The better question is whether the country will make adulthood possible again for people who do not inherit wealth, marry rich, or invent an app that delivers artisanal socks to dogs.

Conclusion

Young people are not doomed, but they are right to feel that the deal has changed. Housing costs, student debt, childcare prices, climate risk, mental health challenges, and shifting job markets have made adulthood more expensive and less predictable than it was for many previous generations. The old advicework hard, save money, buy a house, start a familystill has value, but it no longer works automatically.

The solution is not to mock young adults for delaying milestones. The solution is to understand the real obstacles and build better systems: more affordable housing, stronger entry-level career pathways, practical education options, accessible mental health care, fair wages, climate resilience, and childcare that does not require a treasure map.

Young people are not screwed because they lack talent. They are squeezed because the ladder got taller, the rungs got farther apart, and someone started charging rent for the ground underneath it. The future is still possiblebut it needs more than hustle. It needs policy, community, creativity, and a national willingness to stop pretending that avocado toast caused a housing crisis.