Makeup

How Badly Has The Fed Been Punishing Savers?

Jun

“`

For years, American savers have watched a peculiar financial magic trick. The Federal Reserve lowered interest rates, banks reduced the returns on savings accounts almost immediately, and borrowers celebrated cheaper loans. Then rates rose, borrowing costs shot upward, and many banks responded to depositors with the enthusiasm of a teenager being asked to clean the garage.

That has left millions of people asking a reasonable question: How badly has the Fed been punishing savers?

The answer is more complicated than “the Fed hates your savings account.” The Federal Reserve does not directly set the annual percentage yield on your bank account, nor does it meet eight times a year to discuss how to ruin Grandma’s certificate-of-deposit ladder. Its policies are designed to pursue stable prices and maximum employment.

Nevertheless, those policies can have powerful side effects. During long periods of near-zero interest rates, conservative savers earned almost nothing while inflation quietly reduced the purchasing power of their cash. When the Fed later raised rates, savers finally had opportunities to earn meaningful interestbut only if they were willing to move their money.

The Fed Does Not Set Your Savings Rate, but It Sets the Weather

The federal funds rate is the overnight interest rate targeted by the Federal Open Market Committee. It influences other short-term rates across the financial system, including Treasury bill yields, money market rates, credit card rates, adjustable-rate loans, certificates of deposit, and savings-account yields.

Think of the Fed as controlling the financial climate. It does not decide whether your bank hands you an umbrella, but it has considerable influence over whether it is raining.

When the federal funds rate falls, banks generally reduce the rates they pay depositors. When it rises, savings yields usually increasebut often more slowly and unevenly. Banks with plenty of low-cost deposits may have little reason to offer customers a better deal. Online banks and institutions competing aggressively for deposits tend to react faster.

Why deposit rates lag behind Fed increases

Bank customers are surprisingly loyal to bad savings rates. They may value convenience, dislike opening new accounts, overlook small interest payments, or simply assume every bank pays roughly the same amount. Banks understand this behavior.

Economists describe the extent to which banks pass higher market rates to depositors as the deposit beta. A 100-basis-point Fed increase does not necessarily produce a 100-basis-point increase in every savings account. The pass-through depends on competition, funding needs, account type, customer behavior, and the bank’s business strategy.

That means the Fed may create the conditions for better savings rates without ensuring that your particular bank delivers them.

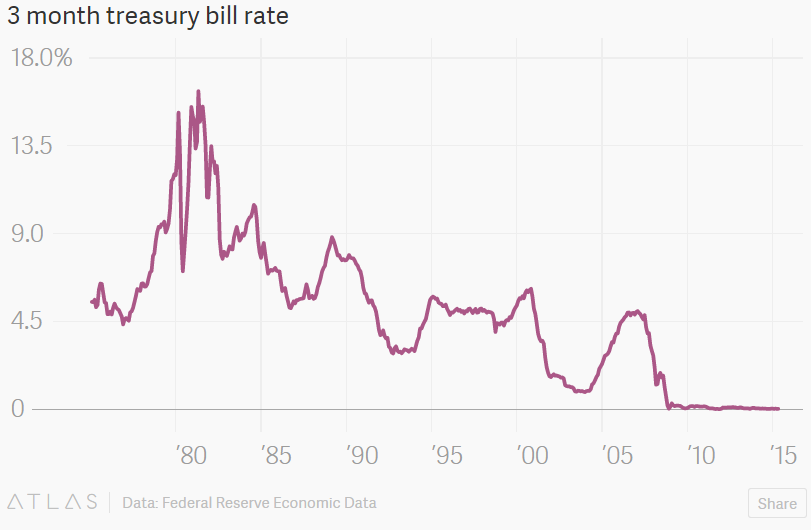

The First Great Squeeze: Near-Zero Rates After 2008

Following the 2008 financial crisis, the Federal Reserve lowered its target range to approximately zero and kept it there until December 2015. The policy was intended to stabilize financial markets, encourage lending, support employment, and prevent a severe recession from becoming even worse.

From a broad economic perspective, there were strong reasons for emergency monetary support. From a saver’s perspective, however, the experience felt like being asked to provide free storage space for the banking system.

Traditional savings accounts frequently paid only a few hundredths of a percentage point. Short-term CDs and Treasury securities also offered historically weak income. Retirees who had expected to live partly on interest were forced to accept lower income, spend principal, delay retirement, or take additional investment risk.

The difference between nominal and real returns

The number printed on a bank statement is the nominal return. What matters economically is the real return, which accounts for inflation.

Suppose a savings account pays 0.10% while inflation runs at 2%. A $20,000 balance earns only about $20 before taxes, while the cost of a representative basket of goods rises by roughly $400. The saver has more dollars at the end of the year, but those dollars buy less.

That is the central complaint about financial repression: interest rates are held below inflation, reducing the real value of safe savings and making government, household, and corporate debt easier to carry.

The Second Squeeze: The Pandemic Rate Reset

In March 2020, as the pandemic disrupted the global economy, the Federal Reserve again reduced its target rate to near zero. Emergency action helped support credit markets and economic activity, but cash returns quickly collapsed.

At first, weak savings rates did not feel especially painful because inflation remained subdued and households were receiving fiscal support. Then inflation accelerated sharply. By 2021 and 2022, many Americans were earning almost nothing on bank deposits while prices for food, housing, transportation, energy, and other essentials were rising rapidly.

This was an unusually harsh combination for cash savers: near-zero nominal yields plus high inflation.

A depositor earning 0.05% during a period of 7% inflation was not merely failing to grow wealth. The purchasing power of that money was shrinking at a dramatic rate. A $50,000 cash reserve could lose thousands of dollars of real value in one year, even though the account balance never visibly declined.

Inflation is polite that way. It does not steal the dollars. It simply sends them back wearing smaller shoes.

How Much Did Savers Lose?

There is no single figure because the damage depends on the amount saved, the account used, the inflation rate, taxes, and the length of time the money remained in cash. Still, simple examples show the scale of the problem.

| Example | Account Yield | Inflation | Approximate Real Result |

|---|---|---|---|

| $25,000 in low-yield savings | 0.10% | 2.00% | About a 1.9% loss of purchasing power before tax |

| $50,000 during high inflation | 0.05% | 7.00% | Roughly $3,475 of purchasing-power erosion |

| $25,000 at the June 2026 national average | 0.61% | 4.20% | Approximately $898 lost to inflation after nominal interest |

| $25,000 in a competitive high-yield account | 4.15% | 4.20% | Close to breaking even before tax |

These examples are simplified. Actual inflation differs by household, interest may compound, rates can change during the year, and interest income may be taxable. Even so, the lesson is clear: a large gap between inflation and a savings account’s APY can materially reduce wealth.

Did the Fed Punish Savers on Purpose?

No. Savers were collateral damage, not the official target.

The Federal Reserve’s mandate is focused on maximum employment and price stability. During recessions and crises, lower rates are intended to stimulate borrowing, investment, hiring, and spending. The central bank is not required to maximize the interest income of depositors.

That distinction matters, but it does not erase the consequences. Monetary policy creates winners and losers. Lower rates can help mortgage borrowers, businesses seeking financing, homeowners refinancing debt, and investors holding assets that rise in value. At the same time, they reduce income for people relying on CDs, savings accounts, money market deposits, and short-term bonds.

The burden is especially noticeable for retirees and highly risk-averse households. A 35-year-old worker may respond to low rates by investing more heavily in stocks. An 80-year-old retiree paying for groceries from interest income has fewer comfortable choices.

Low Rates Also Pushed Savers Toward More Risk

When safe assets provide inadequate returns, investors often move into dividend stocks, longer-term bonds, real estate funds, private credit, or other investments. This behavior is commonly called reaching for yield.

That shift may produce higher long-term returns, but it also introduces volatility and the possibility of loss. Someone who bought a long-term bond fund for additional yield could later experience a substantial decline when market rates rose. Someone who entered the stock market reluctantly could face a downturn at exactly the wrong time.

In other words, low-rate policy did not simply reduce interest income. It changed the risks people felt pressured to accept.

The Fed Finally Raised RatesSo Why Are Some Savers Still Earning Almost Nothing?

Beginning in March 2022, the Federal Reserve launched one of its most aggressive tightening cycles in decades. It raised the target rate 11 times through July 2023, eventually reaching 5.25% to 5.50%.

The Fed later reduced rates during 2024 and 2025. As of June 22, 2026, the target range stands at 3.50% to 3.75% following the June 17 policy meeting.

Those rates are far above the near-zero levels that dominated much of the period after 2008. Yet the national average savings yield in late June 2026 was approximately 0.61%, while competitive online accounts were paying around 4%.

That enormous gap demonstrates that the Fed is only part of the story. Two savers can hold identical balances in federally insured accounts and receive dramatically different amounts of interest.

At a 0.61% APY, $50,000 generates about $305 over one year. At 4.15%, the same balance generates approximately $2,075. That is a difference of roughly $1,770 for completing some paperwork and moving money to a more competitive account.

Customer inertia is profitable. Your bank may not send a cheerful message saying, “Good news! A competitor will pay you six times more.” Banks are funny like that.

Are Savers Still Being Punished in 2026?

The answer depends on where their money is held.

In May 2026, consumer prices were 4.2% higher than a year earlier. Meanwhile, the average savings account paid well below 1%. A depositor accepting the average yield was therefore experiencing a deeply negative real return.

However, leading high-yield savings accounts, short-term CDs, Treasury securities, and certain money market products were offering rates near 4%. Series I savings bonds issued from May through October 2026 carried a 4.26% composite rate, including an inflation-linked component.

Thus, the current environment is not a universal punishment. It is closer to a financial scavenger hunt. Competitive yields exist, but savers must locate them, compare restrictions, and move their money when rates become uncompetitive.

Who Was Hurt the Most?

Retirees depending on interest income

Retirees who wanted principal stability suffered when CDs and savings accounts paid almost nothing. Many had built plans around interest rates that were common in earlier decades. When those rates disappeared, the arithmetic of retirement changed.

People saving for short-term goals

Home down payments, tuition reserves, emergency funds, and money needed within a few years generally should not be exposed to major market risk. Low interest rates left these savers with few attractive alternatives.

Households with limited financial knowledge

Consumers who did not know about high-yield online accounts, Treasury bills, I bonds, or CD ladders were more likely to remain trapped in low-paying products.

People without enough money to diversify

Wealthier households often owned stocks, real estate, and businesses that benefited from easy monetary policy. Lower-income households were more likely to hold a larger share of their financial assets in cash, meaning they received fewer gains from rising asset prices.

What Savers Can Do Without Taking Reckless Risks

Compare APYs regularly

A savings account should not be treated as a lifelong marriage. Review its APY several times a year and after major Fed decisions. Compare it with FDIC-insured banks and federally insured credit unions.

Separate emergency savings from long-term investments

An emergency fund needs liquidity and stability, not heroic returns. Long-term retirement money may need broader investments capable of outpacing inflation. Asking one account to perform both jobs is like asking a refrigerator to double as a race car.

Build a CD or Treasury ladder

A ladder divides money among securities with different maturity dates. Portions become available regularly, reducing the risk of locking an entire balance at an unfortunate rate.

Consider inflation-protected securities

Series I savings bonds and Treasury Inflation-Protected Securities are designed to provide protection against inflation. They have different liquidity rules, tax features, purchase procedures, and market risks, so they should be evaluated carefully.

Watch fees and conditions

A headline APY may apply only to a limited balance, require direct deposit, involve a monthly fee, or fall after an introductory period. The best yield is the yield you can actually keep.

Conclusion: How Badly Has the Fed Been Punishing Savers?

During the near-zero-rate periods following the 2008 financial crisis and the 2020 pandemic shock, the punishment was substantial. Savers received historically weak nominal returns, often lost purchasing power after inflation, and were encouraged to accept risks they might otherwise have avoided.

Still, blaming the Federal Reserve for every miserable savings rate gives banks too generous an alibi. Fed policy establishes the broad interest-rate environment, but financial institutions decide how much of that rate to pass along. Consumer inertia allows many banks to continue paying remarkably little even when market yields are attractive.

The fairest verdict is that the Fed punished passive savers severely during low-rate periods, while bank pricing and customer behavior often extended the sentence. In today’s higher-rate environment, the punishment is increasingly optionalbut escaping it requires attention, comparison shopping, and occasional administrative effort.

What the Fed’s Rate Policy Feels Like to Real Savers

Consider a composite example based on the experiences faced by many American retirees after the financial crisis. Robert and Elaine entered retirement with $300,000 in CDs and savings accounts. They were not trying to beat the stock market. Their goal was straightforward: preserve their principal, collect interest, and avoid turning breakfast into a daily discussion about the S&P 500.

When safe rates were around 4%, their savings could generate approximately $12,000 a year before taxes. That income helped cover property taxes, utilities, insurance, and occasional travel. After short-term rates collapsed, renewing their CDs produced dramatically less income. At 0.50%, the same $300,000 generated only $1,500 a year.

Their principal had not vanished, but their financial plan had lost more than $10,000 of expected annual income. They could spend principal, reduce their lifestyle, buy riskier investments, or hope rates recovered quickly. None of those options felt like the safe retirement they had carefully planned.

Now consider Maya, a younger saver who built a $30,000 emergency and home-down-payment fund between 2020 and 2022. She was proud of avoiding debt and keeping the money safe. Her traditional bank paid approximately 0.01%, producing about $3 of annual interest. Then rent, groceries, used vehicles, and home prices rose rapidly.

Maya’s account statement still displayed $30,003, but the economic value of that money had fallen. The down payment she was chasing moved farther away even though she had done the supposedly responsible thing: worked, saved, and avoided speculation.

After rates increased, Maya assumed her bank would automatically improve her yield. It didbut only slightly. She eventually discovered an online savings account paying several percentage points more. Moving the money required opening an account, linking banks, verifying small deposits, updating beneficiaries, and convincing herself that an unfamiliar online institution with federal deposit insurance was legitimate.

The process was not difficult, but it was inconvenient enough that she had postponed it for months. Once completed, the difference was immediate. A 4% yield on $30,000 produced roughly $1,200 a year instead of pocket change. That did not make her rich, but it covered part of a home inspection, moving expenses, or several weeks of groceries.

These examples reveal why savers often describe Fed policy as punishment. The harm is rarely dramatic on a monthly statement. There is no red warning saying, “Your purchasing power declined today.” Instead, the effect appears gradually through smaller interest payments, more expensive goals, reduced retirement income, and pressure to take unwanted risks.

The modern saver’s experience also contains a frustrating irony. When the Fed cuts rates, banks often lower savings yields quickly. When the Fed raises rates, many institutions wait to see whether customers notice. Savers therefore bear both monetary-policy risk and what might politely be called the “we hope you are not paying attention” business model.

The practical lesson is not to abandon cash. Emergency funds and short-term savings remain essential. The lesson is to make cash compete for its place in your financial plan. Check the APY, calculate the actual dollars earned, compare federally insured alternatives, and measure the return against inflation. Savers cannot control the Federal Reserve, but they can refuse to let an uncompetitive bank turn loyalty into a recurring fee paid through lost interest.

Note: Interest rates, inflation figures, and account yields change frequently. This article provides general educational information rather than individualized investment, tax, or financial advice. Verify current rates, insurance coverage, withdrawal rules, fees, and tax consequences before moving money.